A three-letter trick: Did Kostin and Chemezov deceive UWC investors?

The additional issue of UWC shares could have been a large-scale scam, from which the main shareholders of the VTB and Rostec group were in the black, and the investors who believed them were in the minus.

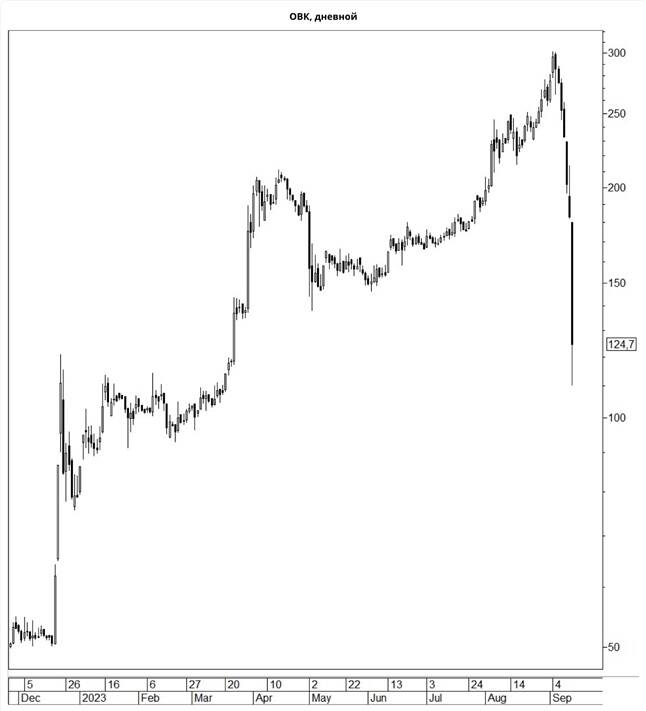

In just five days, from September 8 to 13, shares of the United Carriage Company (UWC) on the Moscow Exchange fell by almost 60%. The reason is said to be the unexpected decision of shareholders to conduct an additional issue of shares. Yes, what – their number will immediately increase 100 times. And according to the laws of the market and common sense, the nominal value of the shares themselves will collapse by the same amount.

Investors who have been actively buying the company’s securities since at least December 2022 have something to be indignant about. The current situation resembles a large-scale scam, from which the current owners of UWC could profit. Among them are Trust, Rostec State Corporation, and Otkritie Bank, controlled by VTB.

Over the past year and a half, UWC pretended that everything was fine. Plans were announced to resume the production of wagons, an agreement was signed for the supply of thousands of grain carriers, and many other “tasty” moments for investors. As a result, since December 2022, UWC shares have almost quadrupled in price.

In August 2023, the alarm bell rang. The company announced that the agenda of the shareholders’ meeting will include the issue of an additional issue of shares – increasing the authorized capital by injecting new funds into it. Accordingly, there are more shares, and their price falls.

In fact, this is a common practice for many companies that lack funds for development. The question is volumes. The decision of the shareholders meeting on September 11 shocked investors: they decided to immediately increase the authorized capital… more than 100 times – from 115 million to 12.5 billion rubles. Accordingly, the cost of one share turned out to be a hundred times lower. This caused a shock on the market and a real collapse in the value of the company.

Dynamics of the price of UWC shares on the Moscow Exchange from December 2022 to September 2023. Photo: https://bcs-express.ru/novosti-i-analitika/aktsii-ovk-obvalilis-na-40-iz-za-korporativnogo-negativa

It’s surprising that UWC’s potential partners didn’t figure out what was going on. Everyone was well aware of past scandals related to the structure. However, investors were not deterred even by the fact that in 2021 the company committed a technical default on its bonds through OVK Finance. Then they could not find more than 15 billion rubles to cover investors’ expenses. Today, OVK Finance is in bankruptcy proceedings with a hole in its capital of 32 billion rubles.

Dynamics of the collapse from September 5 to September 13, 2023. Photo: https://smart-lab.ru/blog/940725.php

Actually, the entire HVAC industry is in the same financial hole. For the first half of 2023, the net loss amounted to 2.9 billion rubles. In 2022, the loss amounted to 22.4 billion rubles, increasing more than 5 times by 2021. And against the backdrop of all this, UWC shareholders put a good face on a bad game?

Financial analysts’ assessments are eloquent. Photo: https://www.tinkoff.ru/invest/social/profile/AkopyanSergey/2b5892c7-49bd-404f-a522-3c1886281e40/

In September 2023, when announcing an additional issue of shares, the company did not even hide the fact that the size of UWC’s financial debt amounted to a considerable 71.7 billion rubles. Moreover, its main part is short-term debt, which will have to be repaid before the end of September (!) 2023. Is this what all the fuss about raising funds through the Moscow Exchange was all about? It must be assumed that something also went to the main beneficiaries of the structure. And after this, the HVAC itself may even be sold.

Who skims the cream

Who makes decisions at UWC today? The main shareholders are known. This is Trust Bank, which is owned by the state and is actually controlled by the Central Bank. In addition, this is Otkritie Bank, which since December 2022 has come under the control of VTB, led by Andrey Kostin. It was from this time that the “pumping up” of investors with promises about the group’s unprecedented plans and prospects began. The current CEO of UWC, Dmitry Olyunin, was Kostin’s first deputy at VTB until 2020. This is not just an ally, but his right hand.

There is a suspicion that the current “multi-move”, which caused a collapse on the Moscow Exchange, may be the work of Andrei Kostin’s team.

Mr. Olyunin’s career path is also interesting. It seems that Kostin is directing him to carry out sensitive assignments. For example, related to plans to take over competitors.

Olyunin has worked for VTB Group since 2004. In 2004-2006 he was vice president of Vneshtorgbank. From February 2006 to December 2007, he served as First Deputy Chairman of the Board of Industrial Construction Bank OJSC. Then he was first deputy president, member of the board, and then head of the board of TransCreditBank OJSC. Afterwards he held senior positions at Rosbank, and then returned to VTB.

Dmitry Olyunin – Andrei Kostin’s “special guarantor” for the absorption of other people’s assets? Photo: https://s0.rbk.ru/v6_top_pics/media/img/8/93/755768576064938.jpg

These banks have one thing in common – they were all absorbed by VTB according to the standard scheme. First, the bank enters into the capital of the structure – for example, by purchasing debts. And then, instead of development and additional capitalization, there is an increase in the share and a banal merger with VTB with the absorption of assets. On the Russian market, Sovcombank is actively involved in similar activities. Moreover, not without the help of the Central Bank, which time after time gives it new structures for rehabilitation. With a well-known result – replenishment of the assets of Dmitry and Sergei Khotimsky.

Nesis came in and left, Rostec stayed

More than 9% of UWC shares are owned by the Rostec state corporation (through Uralvagonzavod) under the management of Sergei Chemezov. The structure received them from the ICT group of Alexander Nesis in 2019. However, in fact, Nesis initially did not go anywhere – he made a “knight’s move.” And while the new owners shared seats on the Board of Directors, he again entered the company’s capital in the same 2019, managing to consolidate more than 12% of the shares in the hands of his team.

True, he did this not directly, but through the “First Heavyweight Company” (PTK), recently purchased from Sergei Generalov, headed by Nesis’s close associate, ex-General Director of UWC Roman Savushkin. At the same time, PTK at that time already owned 1.51% of UWC shares. Other top managers of UWC who worked in Nesis also moved there, to Savushkin – Dmitry Losev, Alexander Filin and others. All of them also took leadership positions.

As Vgudok writes, Nesis and Rostec were friendly towards each other in UWC, having a total of about 20% of the shares. And they had someone to be friends with: after all, Otkritie and Trust still had huge questions for Nesis.

Let us recall that almost immediately after the sale of shares in UWC, on behalf of the company, they filed claims against the ICT Nesis group for 8 billion rubles in the court of Cyprus. Its details remained unknown, however, the press wrote that we were talking about transactions with signs of non-marketability, the purpose of which was the withdrawal of funds. That is, if this is true, this could have been done by the same top management of UWC under the leadership of Nesis, who later moved to PTK.

Going back a little, the deal with Generalov also looks extremely suspicious. In 2017, UWC sold 4.5 thousand innovative railcars to State Transport Leasing Company for 12 billion rubles. But STLC turned out to be only an intermediary, because the final buyer (already for 31 billion rubles) was Sergei Generalov’s Vostok 1520 company. Is that why he gave Nesis the PTK with a calm soul?

Even before this, ICT was rapidly reducing its share in UWC. In 2016-2017, it was already less than 50%, and at the same time the NPF of the Safmar group of Mikhail Gutseriev entered there.

…and Mikhelson who joined them

Then things got more interesting. In the same 2019, when Nesis again found himself in UWC, he abruptly left the capital, selling his shares to Emil Pirumov. The latter is considered to be the man of Novatek owner Leonid Mikhelson. Previously, Pirumov headed GES-2 LLC, which managed the site of the same name (cultural space) on the Bolotoy embankment in Moscow. “GES-2” itself belongs to the VAC Michelson Foundation for Contemporary Art. Now GES-2 LLC belongs to Mikhelson’s daughter Victoria.

There is no information that Pirumov left the capital of UWC. It turns out that the beneficiaries of the current catastrophe with shares could also be Leonid Mikhelson’s people. As for Nesis, he has already received his from the company, and now he is completely withdrawing from Russian assets. It is assumed that the Russian part of the Polymetal business may go to the controversial gold miner Vladislav Sviblov.

All this was known before the September decision of UWC shareholders to conduct an additional issue of shares. Now it makes them neither hot nor cold.

Sergey Chemezov and Andrey Kostin were clearly pleased with the situation with UWC shares. Photo: https://fishki.net/anti/1948657-o-tom-kak-piljat.html

Knowledgeable people point out that after the additional issue of UWC shares, the volume of free-float (their share in free float) may turn out to be so small that the majority shareholder may carry out a forced repurchase. As a result, the company may become non-public, and its shares will cease to be traded on the Moscow Exchange.

Those. The current problems of investors may end in the complete deprivation of their investments for pennies. And for some reason it seems that neither VTB, nor Trust, nor Rostec will be very upset about this. It seems that they have already received theirs in full.

{kind=link}